Setting Goals for Innovation

- Posted by Dan Toma

- On 24/04/2023

Setting goals for the innovation investment is critical if your company treats innovation as a business imperative activity and not just a nice to have that happens on the sideline.

This said, setting goals for innovation becomes even more critical in times when resources are scarce and the company needs to reshuffle its priorities.

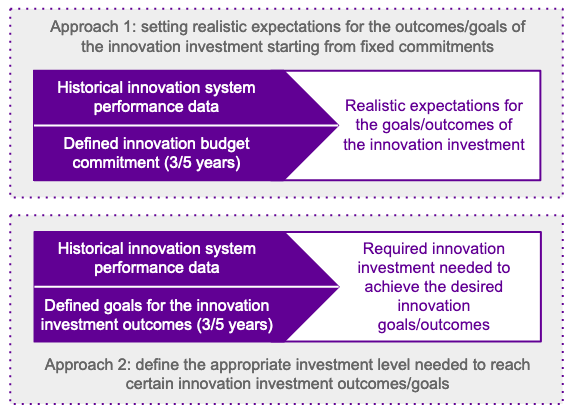

Experience has shown us that, when it comes to setting goals for innovation, leaders are typically interested in finding a concrete answer to one of two questions:

- How much do they need to invest given what they want to accomplish with innovation?

- What is a realistic goal for their innovation efforts given how much they are prepared to invest?

We usually refer to the first question as the Future-to-Present way of setting innovation goals, and to the second question as the Present-to-Future way. One way is not superior to the other and every leadership team picks the one that best suits their company’s context.

Future-to-Present or “How much do we need to invest given what we want to accomplish with innovation?”

To answer the question of the Future-to-Present scenario there are certain data points that are needed.

First and foremost the company needs clarity around what it hopes to achieve through innovation. This can be anything from a certain portfolio mix (percentage of Core Adjacent and Transformational initiative at a certain point in the future) to a certain NPVI (New Product Vitality Index) figure or even a certain top-line growth number.

These figures usually represent a certain commitment the company has made to its shareholders or numbers it needs to hit with innovation given a degrading core business performance.

Secondly, the leadership team must align on the time horizon to achieve the set goals.

Thirdly, the company will need historical data around a variety of innovation accounting indicators such as ACR (Average Funnel Conversion Rate), ATS (Average Time to ‘Sustain’), CoF (Average Cost of Failure) and AR (Average Returns).

With these three inputs and using a bit of basic math, the leadership team can walk backwards from what it wants to achieve in the future, to what it needs to invest today given its past performance.

Take for example a company that wants to obtain $1,000,000 of new revenue in 5 years for their innovation activities. If their ACR is 3.5%, ATS is 2.5 years, average cost of failure is $5,000 and average new revenue per venture is $200,000. Then the company will have to make a $715,000 investment in innovation to achieve its set goals, following the math below:

1,000,000 : 200,000 = 5. Meaning the company will have to have no less than 5 successful ventures in order to hope it will achieve its set goal.

5 : 3.5% = 142.8. Meaning that for the company to hope to have 5 successful venues it needs to kickoff about 143. Given the fact that the company’s ATS is 2.5 years and that it hopes to achieve its $1,000,000 goal in 5 years. The company will have to kick off at least half of the 143 ventures now and the rest no later than 2.5 years from now.

Now, given the company’s average cost of failure of $5,000 per venture, the company will have set aside $715,000 ($5,000 * 143) for innovation.

Present-to-Future or “What is a realistic goal for their innovation efforts given how much they are prepared to invest?”

The Present-to-Future works very similar to the Future-to-Present, only the direction of the math changes. If in the Future-to-Present the budget allocation was the unknown, in the Present-to-Future the end result is the unknown.

To answer the question of the Present-to-Future scenario the following data will be needed:

Firstly, the leadership team needs to align on the time horizon. In essence, deciding when they hope to see the impact of their investment in innovation.

With the time horizon set, the next thing will be to decide how much they want to commit to innovation over the set period.

Once the financial commitment is clear the digging for historical data can start. The team will have to look, at the case of the Future-to-Present scenario for historical performance data around the following innovation accounting indicators: ACR (Average Funnel Conversion Rate), ATS (Average Time to ‘Sustain’), AR (Average Returns) and average investment per venture.

Now with some simple math, the leadership team will get a clear picture of what they can expect from their innovation investments.

Take for example a company that has decided to invest $500.000 in innovation next year. From historical data analysis the company know that:

> In general ventures take about 3 years to reach maturity (sustainable and predictable revenues).

> The ATS figure.

> The company’s ACR is about 4%

> Its average investment per venture is about $10.000.

> And the average returns from an innovation venture are usually $300.000

Therefore, based on the following math, the company can expect to gain $600.000 in 3 years from the investment they are prepared to make this year:

500.000 : 10.000 = 50 Representing the number of ventures the company can kickoff given what the leadership team has set aside for innovation.

50 * 4% = 2 Meaning that the leadership team should realistically not expect more than 2 ventures to reach maturity.

2 * 300.000 = $600.000 (the amount they can expect to gain from the investment in innovation)

Note that in the absence of a company’s innovation accounting data, data from startup accelerator programs or venture capital companies active in the same industry as the company can be used. Although this data needs to be taken with a pinch of salt, it can serve as a decent proxy for the company’s own innovation perforce data.

Many companies today still consider innovation to be more art than science. However, nothing could be further from the truth. If management principles, logic (common sense), discipline and pragmatism are applied to innovation, what was once viewed as art can become a science. Furthermore, clear goals for innovation will have a ripple effect, impacting capability development strategies, organizational structure or hiring policy, just to name a few.

Our innovation accounting and portfolio management tool, SATORI, will help track the necessary KPIs for the goals setting.

Many companies today still consider innovation to be more art than science. However, nothing could be further from the truth. If management principles, logic (common sense), discipline and pragmatism are applied to innovation, what was once viewed as art can become a science. Furthermore, clear goals for innovation will have a ripple effect, impacting capability development strategies, organizational structure or hiring policy, just to name a few.

Visual summary of the article.